Consumers' optimism about their financial future fades as the risk of missing debt payments grows

SAN MATEO, Calif., Nov. 12, 2024 -- The 2024 presidential election thrust voters' financial challenges into the spotlight, with political polling indicating many Americans ranked the economy as the most important issue influencing their vote. A new study by Achieve shows that many Americans simply don't have enough money to make ends meet without turning to debt. For these consumers, concern is growing that they'll soon be unable to meet their monthly financial obligations.

58% of respondents said they are carrying a credit card balance to cover the cost of essential expenses.

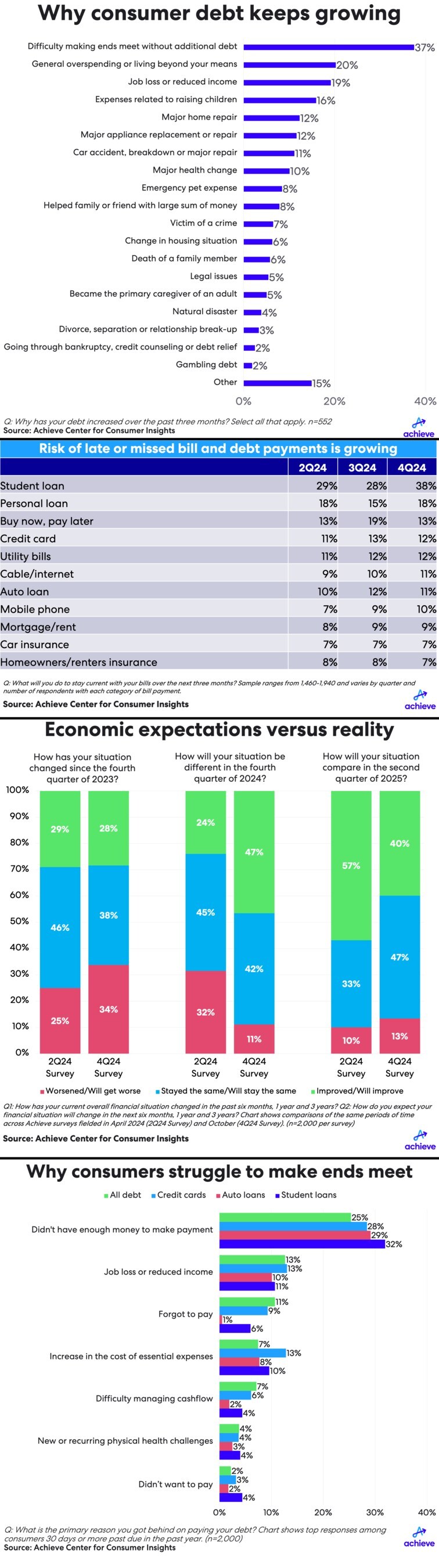

The series of quarterly surveys by Achieve's think tank, the Achieve Center for Consumer Insights, is designed to complement the Federal Reserve Bank of New York's Quarterly Report on Household Debt and Credit. Achieve's survey found that 28% of respondents have seen their debt increase over the past three months. Among those with rising debt, nearly two in five (37%) said the increase is due to the ongoing difficulty of making ends meet, while about one in five attributed their rising debt to both general overspending (20%) and a lost job or reduced wages (19%). Among the 42% of consumers whose total debt hasn't changed over the past three months, 35% attributed it a pattern of paying down some debts, but then incurring new debt, while 21% said they've avoided taking on new debt, but haven't been able to make progress paying down debts they already owe.

Why consumer debt keeps growing | |

Percent of consumers | |

Difficulty making ends meet without additional debt | 37 % |

General overspending or living beyond your means | 20 % |

Job loss or reduced income | 19 % |

Expenses related to raising children | 16 % |

Major appliance replacement or repair | 12 % |

Major home repair | 12 % |

Car accident, breakdown or major repair | 11 % |

Major health change | 10 % |

Helped family or friend with large sum of money | 8 % |

Emergency pet expense | 8 % |

Victim of a crime | 7 % |

Death of a family member | 6 % |

Change in housing situation | 6 % |

Became the primary caregiver of an adult | 5 % |

Legal issues | 5 % |

Natural disaster | 4 % |

Divorce, separation or relationship break-up | 3 % |

Gambling debt | 2 % |

Going through bankruptcy, credit counseling or debt relief | 2 % |

Other | 15 % |

Q: Why has your debt increased over the past three months? Select all that apply. n=552 Source: Achieve Center for Consumer Insights | |

Risk of missed payments grows

During the fourth quarter, 36% of respondents said it's very difficult or difficult for them to pay their recurring debts on time, unchanged from the third quarter. Among these respondents, 68% said paying their debts on time is a challenge because they don't make enough money to cover their spending, up from 64% one quarter ago.

"Across the board, unemployment is low and wages have risen, but those macroeconomic conditions aren't felt equally across the population, especially for consumers who live in areas where the impact of inflation is the greatest," said Achieve Co-CEO and Co-Founder Brad Stroh. "More than a quarter of Americans are seeing their amount of debt increase and a majority don't have enough money to cover their spending month to month. The slippery slope of debt will increase for many households if they don't take steps to realign their finances."

The share of respondents who said they are carrying a credit card balance to cover the cost of essential expenses was 58%, including 29% who said spending on living expenses has accrued on their credit card balances for more than six months. The effect of this financial stress is increasing, as respondents indicate that they are at greater risk of missing a bill or debt payment in the coming months. For example, in Achieve's fourth quarter survey, 38% of respondents with a student loan said they believe they will be late or miss a payment. That's a significant increase from prior surveys. Smaller increases in late and missed payment risk is also occurring in bill payment categories that many view as absolutely essential for daily life, like mobile phones and internet access.

Risk of late or missed bill and debt payments is growing | |||

Debt Type | 2Q24 | 3Q24 | 4Q24 |

Student loan | 29 % | 28 % | 38 % |

Personal loan | 18 % | 15 % | 18 % |

Buy now, pay later | 13 % | 19 % | 13 % |

Credit card | 11 % | 13 % | 12 % |

Utility bills | 11 % | 12 % | 12 % |

Cable/internet | 9 % | 10 % | 11 % |

Auto loan | 10 % | 12 % | 11 % |

Mobile phone | 7 % | 9 % | 10 % |

Mortgage/rent | 8 % | 9 % | 9 % |

Car insurance | 7 % | 7 % | 7 % |

Homeowners/renters insurance | 8 % | 8 % | 7 % |

Q: What will you do to stay current with your bills over the next three months? Sample ranges from 1,460-1,940 and varies by quarter and number of respondents with each category of bill payment. Source: Achieve Center for Consumer Insights | |||

Optimism wanes despite financial improvements

In Achieve's fourth quarter 2024 survey, 47% said their financial situation has improved over the past six months. That's nearly double the 24% of respondents from Achieve's second quarter 2024 survey who expected their situation to improve over this time. Similarly, 32% of 2Q24 survey respondents expected their situation to worsen over the coming six months. But among 4Q24 respondents looking back over that time, just 11% said their financial situation deteriorated. Looking ahead, 40% of 4Q24 survey respondents expect their financial situation to improve in the second quarter of 2025, down from 57% of 2Q24 survey respondents who said they expect to see an improvement at the same period of time.

Economic expectations versus reality | ||||

Worsened/Will get worse | Stayed the same/Will stay the same | Improved/Will improve | ||

How has your situation changed since the fourth quarter of 2023? | 2Q24 Survey | 25 % | 46 % | 29 % |

4Q24 Survey | 34 % | 38 % | 28 % | |

How will your situation be different in the fourth quarter of 2024? | 2Q24 Survey | 32 % | 45 % | 24 % |

4Q24 Survey | 11 % | 42 % | 47 % | |

How will your situation compare in the second quarter of 2025? | 2Q24 Survey | 10 % | 33 % | 57 % |

4Q24 Survey | 13 % | 47 % | 40 % | |

Q1: How has your current overall financial situation changed in the past six months, 1 year and 3 years? Q2: How do you expect your financial situation will change in the next six months, 1 year and 3 years? Chart shows comparisons of the same periods of time across Achieve surveys fielded in April 2024 (2Q24 Survey) and October (4Q24 Survey). (n=2,000 per survey) Source: Achieve Center for Consumer Insights | ||||

Why consumers fall behind on their debts

Consumers who do become delinquent on their debts cite a number of reasons for missing payments, but the most oft-cited reason comes down to not having enough money to make their payment. Across all debt types that Achieve tracks, 25% of respondents cited this as the primary reason they missed a payment, while 32% of student loan borrowers who recently missed a payment also cited this reason. Job losses and reduced income are another significant cause across all debt types, ranging from 10% to 13%, depending on the debt category. Additionally, 11% of respondents with a missed payment across all debt categories said they forgot to pay.

Why consumers struggle to make ends meet | ||||

Reasons for late or missed payment | Student loans | Auto loans | Credit cards | All debt |

Didn't want to pay | 4 % | 2 % | 3 % | 2 % |

New or recurring physical health challenges | 4 % | 3 % | 4 % | 4 % |

Difficulty managing cashflow | 4 % | 2 % | 6 % | 7 % |

Increase in the cost of essential expenses | 10 % | 8 % | 13 % | 7 % |

Forgot to pay | 6 % | 1 % | 9 % | 11 % |

Job loss or reduced income | 11 % | 10 % | 13 % | 13 % |

Didn't have enough money to make payment | 32 % | 29 % | 28 % | 25 % |

Q: What is the primary reason you got behind on paying your debt? Chart shows top responses among consumers 30 days or more past due in the past year. (n=2,000) Source: Achieve Center for Consumer Insights | ||||

Methodology

The data and findings presented are based on an Achieve survey conducted in October 2024 consisting of 2,000 U.S. consumers ages 18 and older with an active account for one or more of the following categories of consumer debt: auto loan; major credit card with a minimum outstanding balance of $100; first-lien mortgage; home equity line of credit (HELOC); student loan; and other (unsecured personal loan, store-branded credit card, buy now, pay later loan, or closed-end home equity loan). The sample was augmented to include a statistically significant subset of credit card, auto loan and student loan borrowers who have been 30 days or more past due at least once in the past six months.

About the Achieve Center for Consumer Insights

The Achieve Center for Consumer Insights is a think tank that leverages Achieve's team of digital personal finance experts to provide a view into the state of consumer finances. In addition to sharing insights gleaned from Achieve's proprietary data and analytics, the Achieve Center for Consumer Insights publishes in-depth research, bespoke data and thoughtful commentary in support of Achieve's mission of helping everyday people get on the path to a better financial future.

About Achieve

Achieve, THE digital personal finance company, helps everyday people get on, and stay on, the path to a better financial future. Achieve pairs proprietary data and analytics with personalized support to offer personal loans, home equity loans, debt resolution and debt consolidation, along with financial tips and education and free mobile apps: Achieve MoLO® (Money Left Over) and Achieve GOOD™ (Get Out Of Debt). Achieve has 2,500 dedicated teammates across the country, with hubs in Arizona, California, Florida and Texas. Achieve is frequently recognized as a Best Place to Work.

Achieve refers to the global organization and may denote one or more affiliates of Achieve Company, including Achieve.com (NMLS ID #138464); Achieve Home Loans, Equal Housing Lender (NMLS ID #1810501); Achieve Personal Loans (NMLS ID #227977); Achieve Resolution (NMLS ID # 1248929) and Freedom Financial Asset Management (CRD #170229).

Contact

Erica Bigley

Vice President

Corporate Communications

ebigley@achieve.com

415-710-9006

Austin Kilgore

Director

Corporate Communications

akilgore@achieve.com

214-908-5097

This News is brought to you by Qube Mark, your trusted source for the latest updates and insights in marketing technology. Stay tuned for more groundbreaking innovations in the world of technology.